http://www.ft.com/cms/s/2/bd754d1a-2a45-11e5-acfb-cbd2e1c81cca.html#axzz3kVP2nAF8

Last

updated: July

29, 2015 4:07 pm

China seeks

confirmation of renminbi’s arrival on world stage

·

Share

·

Author alerts

·

Print

·

Clip

·

Comments

The

IMF's managing director Christine Lagarde

If, 20 or 30 years from now, central banks and sovereign wealth

funds hold a significant portion of their reserves in renminbi-denominated assets,

financial historians will probably look back on 2015 as a turning point.

The International Monetary Fund is engaged in a year-long review

of the currency composition of its special drawing

rights (SDR), with a final decision expected

between November and early 2016. The currencies now included in the SDR

“basket” are from the world’s most influential economies: dollars, euros, yen

and sterling.

If the fund decides to add the renminbi to the SDR basket, it will amount to an assurance to

global central banks by the world’s foremost financial technocrats that

renminbi assets are safe.

For China, inclusion in the SDR would also symbolise

the arrival of its currency on the world stage alongside those of the world’s

richest countries. National leaders would see it as a sign of respect for

China’s increased influence in the world economy and the reforms it has taken

to integrate itself with the global financial system.

“SDR inclusion could be interpreted as international recognition

of China’s increased economic importance and role in global financial markets,”

says Zhu Haibin, chief China economist at JPMorgan Chase.

The direct impact of SDR inclusion is almost negligible. The IMF created SDRs in 1969 to

respond to a global shortage in viable reserve assets under the Bretton Woods

system of fixed exchange rates. But Bretton Woods collapsed less than a decade

later and today various currencies not included in SDRs, such as the Swiss

franc and Australian dollar, are also widely held as reserves.

“While it appears to be a contentious issue, the Rmb’s inclusion

in the SDR has little tangible and immediate economic benefit for China. The

SDR is rarely used by the global financial markets and no country would manage

foreign exchange reserves modelled by the SDR,” says Li-Gang Liu, chief greater

China economist at Australia and New Zealand Banking Group.

But inclusion into this elite club would have real-world

consequences. Every IMF member holds at least some SDRs. Thus, the inclusion of

the renminbi would mean that these countries would suddenly be holding

renminbi, albeit indirectly. With that threshold crossed, central bank renminbi

holdings could be poised to increase rapidly.

Though there is no formal application process to join the SDR

basket, China has clearly stated its desire to be included as a result of the

five-yearly review now under way.

Wei Yao, China economist at Société Générale who assesses the

renminbi’s chances of inclusion at about 50 per cent, says: “China, as the

biggest exporter in the world, passes the first test with flying colours. It is

more debatable whether the renminbi meets the second criterion.”

The main sticking point is Chinese capital controls, which

severely restrict buying and selling of renminbi for investment purposes.

Progress on so-called capital-account

convertibility will be an important

factor in the IMF’s decision.

The launch of the Shanghai-Hong Kong

Stock Connect last November marked

an important step towards allowing freer cross-border flows of renminbi —

known as capital-account liberalisation. But the programme is still subject to

a quota that caps foreign investment to a tiny fraction of overall market

capitalisation.

Access to the bond market is an even greater obstacle, as bonds

are the favoured assets for central bank reserve managers. China took an

important step towards free usability in July, however, when it announced that

central banks and sovereign wealth funds no longer needed preapproval to buy

into the domestic bond market. But non-official

investors such as mutual funds and individuals remain subject to quota and

licensing restrictions.

“The announcement

shows that the PBoC’s determination for capital-account liberalisation has not

been deterred by the stock market volatility . . . and that the central

bank is still promoting the renminbi’s inclusion in the IMF’s SDR basket during

its next review,” said Jianguang Shen, China economist at Mizuho Securities

Asia.

The IMF has never adopted specific metrics to determine whether a currency

is “freely usable”, giving the fund’s executive board considerable flexibility.

However, unofficial IMF working papers suggest that the fund considers whether

the renminbi is, in fact, widely used for financial transactions at least as

important as what regulations appear to permit or forbid.

“Capital-account convertibility is not a precondition for SDR

inclusion. For instance, the yen was included in the SDR basket in 1973, but

Japan liberalised international capital flows only in 1980,” says Mr Zhu.

In this regard, the fact that 60 central banks already hold

renminbi among their reserves, according to Standard Chartered estimates, is

likely to be viewed as an important indicator of usability. But it remains

unclear how the IMF will interpret the fact that many of these central bank

reserves are held in offshore renminbi assets, which are not subject to Chinese

regulations.

Many other obstacles remain to the currency being “freely usable”.

Individuals are still subject to a $50,000 per year limit on converting

renminbi to foreign currency and vice versa. China plans to roll out a pilot

programme for individual outbound investment this year, but it will still be

subject to quotas.

Ultimately, analysts expect political considerations to play an

important role. If the fund refuses entry to China, it could deepen the Chinese

leadership’s distrust of institutions such as the IMF, World Bank and G20,

which it already views as unfairly dominated by the west.

On the other hand, the US is likely to argue that the SDR is an

important lever that can be used to incentivise China to quicken financial

reform. IMF president Christine Lagarde has said that the renminbi’s inclusion

is a “matter of when, not if”. That has led many observers to expect a

compromise in which the fund will formally declare its intention to add the

renminbi to the SDR — but only once deregulation proceeds a bit further.

http://www.ft.com/cms/s/2/4b9725c8-15d3-11e5-be54-00144feabdc0.html#axzz3kVP2nAF8

Last

updated: July

29, 2015 4:07 pm

Battle is on for

offshore renminbi market

For a sense of how the use of the renminbi is expanding beyond China, it helps to turn to Sanchuan Holding Group,

a Chinese hydropower company.

The company is not a household name outside China and probably not

much beyond its home base of Hangzhou, a city in eastern China.

But it recently signed up United Overseas Bank in Singapore to

handle its cross-border renminbi cash management, to support expansion beyond

China.

Lin Jianhua, Sanchuan chief executive, says the Singapore bank

approached his company when it learnt that the hydropower group was looking to

extend its operations.

“Recognising that we needed to enhance our cross-border liquidity

flow, UOB shared with us their strong understanding and insight on China’s

financial liberalisation and RMB internationalisation trends, as well as on

offshore RMB regulations,” Mr Lin says.

UOB, Singapore’s third-largest bank by assets, has particularly

strong connections with ethnic Chinese business in the region, as it traces its

roots back 80 years to the Straits Chinese, or Peranakan, who settled in

Southeast Asia in the late 19th century.

It is now acting as intermediary for a next wave of outbound

Chinese businesses such as Sanchuan and doing so by offering renminbi banking

services as Singapore’s role as an offshore renminbi centre grows.

Sam Cheong, head of the foreign direct investment advisory unit at

UOB, says almost half the companies that the bank helps expand into Southeast

Asia are from China. “Increasingly, we are seeing more of them use renminbi as

a settlement currency.”

In June, UOB established a “renminbi solutions team” to help

companies better manage their cross-border business in the Chinese currency.

While Hong Kong remains the dominant offshore renminbi centre,

China has appointed renminbi clearing banks in Singapore, London, Luxembourg

and Taipei and other locations, at the same time agreeing currency swap lines with other central banks and handing out renminbi

quotas.

When it comes to handling global payments in the Chinese currency, the addition of other

countries on top of market leader Hong Kong as renminbi centres boosted the

share of collective activity by such hubs to 25 per cent of total activity in

February. According to Swift, the clearing system, this was up from 17 per cent

in February 2013.

While that may create an impression that each centre is competing for

a slice of offshore renminbi action, the example of Sanchuan shows that each

hub is fulfilling different roles and that they are not necessarily competing

directly with each other, even as the total pie is growing.

Singapore, for example, is building itself up as a regional

treasury centre for multinational companies, as well as companies emerging from

within the Association of Southeast Asian Nations (Asean) and expanding beyond

their home markets.

It is also vying with Hong Kong for pole position as Asia’s

largest wealth management centre.

“Singapore provides a lot of hedging and liquidity solutions for

corporates and is developing wealth management products catering for the

potential opening up of overseas outbound investment for Chinese investors,” says

Candy Ho, global head of renminbi business development, markets, at HSBC in

Hong Kong. “Each of these centres serves different purposes.”

The renminbi has outstripped the Japanese yen, the US dollar and

the Hong Kong dollar as the main currency for payments between China and the

rest of the Asia-Pacific region over the past four years, according to data

from Swift published in May.

The Chinese currency was used in January-April for 31 per cent of

payments between China (including Hong Kong) and the rest of the Asia-Pacific

region, up from 7 per cent back in April 2012, Swift says.

Singapore is increasingly seen as providing a conduit for use of

the renminbi in Southeast Asia, building on the Asian city state’s position as

a regional entrepot since the 19th century.

Meanwhile London, the world’s largest foreign exchange trading

hub, has carved out a role as a big renminbi FX trading centre. In its latest

half-yearly survey of the British capital as a renminbi centre, the City of

London Corporation found “particularly strong growth” in FX-related businesses

in 2014.

Overall trading volumes more than doubled last year, up 143 per

cent, from 2013, with average daily volumes reaching $61.5bn, nearly six times

as large as those reported in the Corporation’s first survey in 2011.

According to the British Consulate in Hong Kong, London accounted

for 42 per cent of all FX trading in renminbi by the third quarter of 2014,

compared with 31 per cent at the end of 2013. This equals the share of such

trades taking place in Hong Kong.

In Taiwan, interest in the renminbi is largely domestic, focusing

on the needs of insurance companies for longer-dated borrowing using so-called Formosa bonds, denominated in

renminbi.

But the underlying trend is clear. Internationalisation of the

renminbi is being driven by the growing number of offshore centres other than

Hong Kong.

Just as in the case of Sanchuan, that process is bringing to light

some unexpected players. Recent data from Swift show that the renminbi is

starting to be used in South Africa, a country hitherto scarcely known for

this.

The amount of payments in the Chinese currency has jumped by a

third in the past 12 months and by 191 per cent over the past two years. According

to Hugo Smit, head of Africa south at Swift: “The rise of renminbi usage in

South Africa is another good indicator of the cross border use of the

currency.”

http://www.ft.com/cms/s/2/29ee3136-1ffc-11e5-ab0f-6bb9974f25d0.html#axzz3kVP2nAF8

Last

updated: July

29, 2015 4:07 pm

Trade propels

renminbi on route to global reserve currency

·

Share

·

Author alerts

·

Print

·

Clip

·

Comments

Russia's

President Vladimir Putin greets Xi Jinping, president of China. Russian

companies have a keen interest in the Rmb

When discussing the internationalisation of China’s renminbi, Denis Shulakov, first vice-president of

Gazprombank in Moscow, is fond of quoting Wayne Gretzky, the former Canadian

ice hockey player and coach.

“You don’t need to be where the puck is, you need to be where the

puck is going to be,” he says.

Gazprombank, like many Russian banks, is furiously working to set

up operations in both Hong Kong and on the Chinese mainland in preparation for

conducting more trade and finance in China’s renminbi: “All the Russian

corporates who are key clients of the bank are moving in this direction,”

explains Mr Shulakov, who says his organisation expects to be the first Russian

bank to obtain a broker dealer licence in Hong Kong.

There is a good reason why Russian companies would be showing a

keen interest in China’s currency for both trade settlement and finance: sanctions

against Russia have frozen access to funds in the west. But for other banks and

companies around the world, the reasons are just as compelling.

The past five years have seen a surge into the renminbi as a way to settle trade with the world’s largest

exporter, a trend enthusiastically supported by Beijing as a means to push its

long-declared goal of having a global reserve

currency, commensurate with the dollar, the yen and the euro.

Already 22 per cent of China’s trade is being settled in renminbi,

up from 8 per cent in 2012 and zero five years ago, according to estimates by

Citi.

Bruce Alter, head of trade and receivables finance for HSBC in

China, reels off a list of companies that he has worked with to do deals in

renminbi: an Australian seafood exporter, a Malaysian palm oil producer, a

Chinese bus manufacturer selling to Brazil and a Canadian furniture retailer.

“If you look at Rmb trade flows 2-3 years ago, it was really

dominated by Hong Kong China trade, but you see today, although there is still

a lot of Hong Kong in the mix, there are more companies from more markets

getting into the Rmb game,” he says.

He says the main benefit of using the renminbi is that for large

importers (often retailers) it is cheaper – it removes the foreign

exchange margin from the contract and often Chinese companies will offer a

discount of 1-2 per cent if buyers pay in renminbi.

As for overseas sellers, agreeing to trade in renminbi gives them

a better chance of penetrating the Chinese market. One additional motivation is

that if overseas sellers already have operations in China, they can use the

renminbi export proceeds to cover their Chinese operational costs.

In addition to hubs such as Hong Kong, Singapore and London, many

more countries are now also involved in offshore renminbi, with China actively

promoting greater adoption of its currency in trade and finance. Central banks

in countries as far apart as Malaysia, Nigeria and Chile hold part of their

foreign exchange reserves in renminbi. The People’s Bank of China (PBoC) has

set up dozens of arrangements with its counterparts around the world, allowing

it to swap renminbi for those parties’ currencies.

“On the trade and commerce aspect, the currency is fully liberal,”

says Sandip Patil, Citi’s Asia managing director for global liquidity and

investments. “Any company can use Rmb whichever way they like to conduct

international trade and associated working capital financing.”

He adds: “Many times you are able to negotiate larger discounts

with your suppliers if you are paying in Rmb” because paying in foreign

currency creates procedural bottlenecks and delays.

But compared with its surging use in trade, the renminbi still has

little take-up in capital markets, despite concerted efforts by the Chinese

government. This is mainly because of continuing restrictions on the ability to

convert and transfer the currency.

Once it obtains a broker licence in Hong Kong, Gazprombank is keen

to access what it estimates to be a $6tn pool of finance in the onshore China

market through “panda bonds”, Chinese renminbi-denominated bonds issued in

China by a non-Chinese issuer. “The only problem with the yuan is conversion

and transfer,” says Mr Shulakov. “If you have onshore yuan you cannot freely

convert it and transfer it.”

Zhou Xiaochuan, China’s central bank governor, has said it is

committed to liberalising China’s capital account, but stops short of wanting

the renminbi to be fully and freely convertible in capital markets

transactions. In a speech in April, Mr Xiaochuan used the term “managed

convertibility”.

Meanwhile, discussion with the International Monetary Fund over

including the renminbi in the basket of currencies used to denominate the IMF’s

special drawing rights (SDR) would open the way for reserve currency status, if

the Fund gave a green light during its five year review in November. But many

are sceptical that this will happen.

Dennis Tan, foreign exchange strategist for Barclays, said China

has met only a few of the prerequisites for being an SDR currency and that the

low usage of Rmb in international financial transactions is a potential

hindrance. “In volume of trade flows and exports, obviously China has made it

into the club,” he says, But in other measures, such as currency denomination

of international banking liabilities and or global reserves, the Rmb still

falls short, he says.

Mr Shulakov, though, is optimistic. “We are yet to experience the

opening up of the Chinese local market,” he says, “but it is going to happen,

inevitably. So we are in discussions and we are preparing ourselves for this,

just as the Morgan Stanleys and Goldman Sachs of this world are doing.”

http://www.ft.com/cms/s/2/4ed5a142-15d3-11e5-be54-00144feabdc0.html#axzz3kVP2nAF8

Last

updated: July

29, 2015 4:07 pm

Renminbi: What lies

ahead?

Li Keqiang did not shirk the issue of currency wars when he spoke to the

Financial Times in April.

“We don’t want to see a scenario in which major economies trip

over each other to devalue their currencies. That would lead to a currency

war,” said China’s premier.

Currency intervention is an issue that has chilled US-China

relations for more than a decade and, while it has gone quiet of late, it is

threatening to resurface.

China’s equity market

shock,

which from mid-June saw a wipeout of more than 30 per cent of the value of

shares in Chinese companies, prompted a dramatic reaction from Beijing with

regulators imposing a six-month ban on share sales by big shareholders.

As China’s economy slows, could another strident reaction be

forthcoming, by depressing the value of the renminbi in order to stimulate trade, in other words a breakout of

the very currency war China has pledged not to

undertake?

This depends on assessing the fair value of the renminbi. The

currency was pegged to the dollar until 2005, since then Beijing has allowed it

to rise, except for a two-year period around the global financial crisis.

From the end of the peg to the end of 2013, it rose in value

against the dollar by a third.

After the dollar hit a low of Rmb6.05, the currency pair has for

the past 18 months traded in a band of Rmb6.05 to 6.27.

That, according to Aroop Chatterjee, foreign exchange strategist

in Barclays, is where Beijing wants the renminbi to stay for a number of

reasons.

Chief among them is Beijing’s campaign to be included in special drawing

rights (SDR) the basket of currencies afforded

official reserve currency status by the International Monetary Fund. A decision

is expected later this year.

“Part [of the reason for the tight range] is related to the

People’s Bank of China’s intention to keep the renminbi stable and a lot of

that is related to the potential for destabilising capital outflows,” says Mr

Chatterjee.

“But there is also the political intent on SDR. They want to

project a picture of stability to the IMF and the rest of the world.”

For these reasons, several currency strategists expect the

renminbi to hang around the level of Rmb6.26 by the end of the year. But Daniel

Tenengauzer, emerging markets forex strategist at RBC Capital Markets, demurs.

He thinks Beijing will allow the band to widen.

“Part of the internationalisation of the renminbi is a widening of

the band and a more volatile exchange rate,” he says.

This opens up the debate on the renminbi’s valuation. The

International Monetary Fund, in a notable statement in May, declared that it no

longer believed the renminbi was undervalued.

Where the value of the renminbi goes depends on China policy. Mr

Gu reckons it will rise if China accepts lower growth and opens its capital

account to global investors.

But if it chooses to expand fiscal stimulus to support growth and

continues to distort investment, he believes the current account surplus will

shrink quickly and the renminbi will weaken.

Ying Gu, Hong Kong-based emerging markets strategist for JPMorgan,

agrees, particularly as China’s current account surplus to GDP, an indicator

for the currency’s valuation, has fallen to 2.3 per cent.

As the dollar strengthens through US Federal Reserve interest rate

liberalisation, “I am afraid renminbi will become too expensive”, he says.

It already is, says Mr Tenengauzer. “A year ago, the currency was

at fair value and now it’s 15 per cent overvalued,” he says.

Mr Chatterjee agrees. “The dollar has appreciated against the rest

of the world but the dollar-renminbi pair has gone sideways. The renminbi is

quite expensive,” he says.

China’s economy is showing weakness, the country faces

deflationary pressures and the shock sell-off in its equity markets points to

the government needing to find ways to stabilise growth and minimise risks.

Cuts in interest rates are likely.

Whether that amounts to a currency war is a question of

interpretation.

“In the near term, the focus is on SDR,” says Mr Chatterjee. “But

further down the road, the risk to growth is to the downside. With broader

dollar strength, weak growth will lead policymakers to accommodate a weaker

exchange rate.

“If it was the case that the renminbi was moving because of

intervention efforts, that would be different. But there are clear signs in

capital outflows, in the weak economy and in weak inflation that the

macroeconomic backdrop supports a weaker currency.”

http://ftalphaville.ft.com/2015/07/17/2134607/this-isnt-the-chinese-capital-account-liberalisation-youre-looking-for/

This isn’t

the Chinese capital account liberalisation you’re looking for

Author alerts

The broad narrative of a coming capital

account liberalisation in China has always bugged us. The main reason being

that we couldn’t see how China, in its current state, was going to start

letting money flow (easily) out as well as in.

But before we get into that we should note,

somewhat counterintuitively, that China’s capital account is already fairly

liberalised.

As Gavekal’s Chen Long says:

It is not at all easy to specify just how open

a country’s capital account might be. The well-known Chinn-Ito

Index shows that China’s capital account is among the most closed in the world,

and has not opened at all in recent years. Yet this is difficult to square with the fact that

total crossborder capital flows have increased by ten times over the past

decade to US$1.5trn. China has a low level of de jure openness but a higher

level of de facto openness.Very few types of capital flows are

completely free of government control, but the partial controls still allow for

a good deal of flexibility. Foreign direct investment has been largely open for

decades, though there is still an approval process as well as restrictions on

many sectors. Trade credit and offshore borrowing are subject to controls for

prudential reasons, but they are relatively accessible for many companies. More

recently, China has also simplified foreign exchange regulations to give

companies more freedom in dealing with their foreign currency assets. According

to the IMF’s classification, 35 out of 40 capital account items are already

fully or partly convertible in China, leaving only five inconvertible.

The biggest remaining restrictions on capital flows today are on foreign

currency exchange for individuals, and inward and outward portfolio investment.

But there has already been fairly substantial change on this front. Today every

Chinese individual is allowed to buy no more than US$50,000 worth of foreign

currency from banks each year. But that limit was lifted from US$20,000 in

2007, and it is also not that hard for the more savvy to get around it.

Indeed. And if you are a less than savvy

individual you might want to look into hard-to-value assets (such as art work),

insurers, equity deals, Macau, brokerages, underground banks, cruise lines,

and… er, “ants moving houses”.

To savvy up, that is, even if we’d suggest our list is almost certainly lagging

Chinese innovation where this is concerned.

Where the portfolio investment channels are

concerned — mostly quota-based via the Qualified Domestic Institutional

Investor and (RMB) Qualified Foreign Institutional Investor routes —

suffice to say for now, as Long does, that it’s “a more nuanced tool than an

on-off switch, as the quota can be increased over time as regulators get more

comfortable with capital flows. Indeed, since 2012 China has significantly

increased the size of the quotas for each of the channels”, including the

recent Shanghai-Hong Kong Stock Connect which doesn’t apply a quota to

individuals as do the QDII/ QFII and RQDII.

So we’re in a situation where China’s capital

account is more open than it has been before and recent relaxations of control

have increased the size and volatility of flows. Including, obviously but

crucially, outflows. That makes China’s leaders v nervousand restricts policy options.

In fact, suggests Long, that’s one of the

main, again counterintuitive, arguments for liberalisiation:

In fact one of the stronger arguments for further liberalization of

capital flows is that the current situation is an unhappy halfway house:

capital flows have become much larger, but are not very transparent. With some channels quite open but others still closed,

there is much illicit use of the more open channels to disguise capital flows. For instance, companies can falsify export and

import invoices, or trade finance documents, in order to move money in and out

of the country. Reformers argue that it

would be better for these capital flows to happen out in the open rather than

underground. So the debate is not about whether or not to open the capital

account, because it is in fact already partially open. The question is where to

go from here.

We really like this way of looking at the

issue. It’s not naive, for one.

The naive approach sees China marching towards

actual capital account liberalisation. But, seriously, who thinks that is on

the cards in the near term? (Or even, depending on your level of pessimism about

China’s economic future, in the longer term?)

To re-re-re-iterate, this is a system very badly. It is happy to welcome it

in, vastly less happy to see it (now internal capital?) leave. More so, it

doesn’t take much to draw a lesson about attitudes to control and stability

from China’s reaction to the recent stock market puke.

Long argues that the issue of CA

convertibility is high on the politically important list, for both Xi and PBoC

governor Zhou. And that it’s one way for the leadership to demonstrate reform.

Damp squibs elsewhere need to be covered up after all.

Then there’s the SDR angle. The idea of SDR

inclusion has been held up as a status thing in China and for the RMB to included

in the IMF’s currency basket it has to be “freely usable”.

The reality is the decision will be more about

politics and the US’s opinion on the matter — as the IMF noted

previously, “there is no Board-approved set of indicators for such an

assessment, nor a formal limit on the number of currencies that can be

considered freely usable” and that decisions about the basket “would require

judgement framed by the definition of a freely usable currency” — but

here’s a chart from Cap Econ attempting to summarise China’s current position

from a purely economic standpoint:

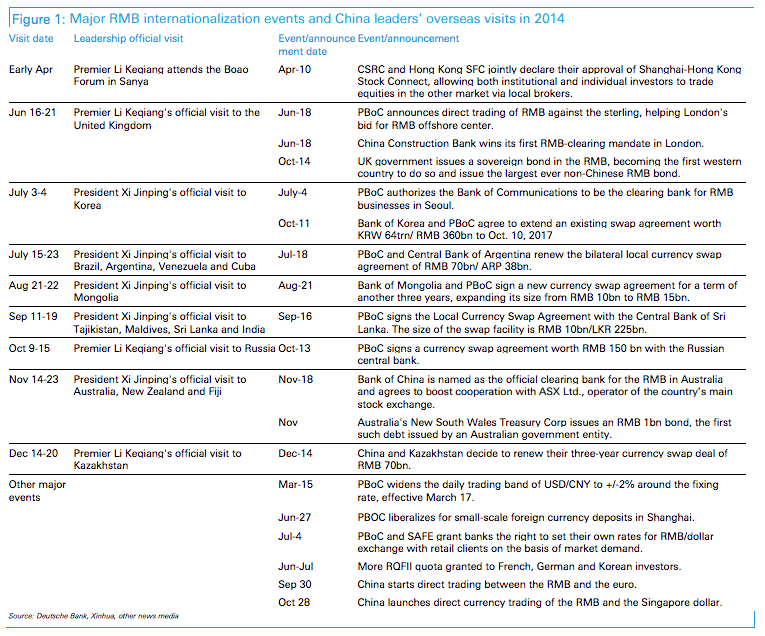

And an extra large chart covering RMB

promotion from Xi et al from Deutsche for those who can be bothered clicking:

The more important political stuff is trickier

to read but do remember that Jack Lew said, per Cap Econ again, on 31st March

that further reforms were needed for the renminbi to qualify to be part of the

SDR basket. So this could well be pushed out either way. Fwiw, Deutsche see a

40 per cent probability that the RMB will become an SDR currency in 2015, and a

70 per cent probability that this will happen by the end of 2016. We shall see.

Anyway, on we go, as this isn’t all about SDR

inclusion and China needs inflows to help with its fiscal problems. Deutsche

estimated in April that the size of the central government’s financing gap may

be 3.7 per cent, and, to give one example, it could do with generating external

demand as it launches its local government debt swap plansin

ever greater style. For those keeping count, another RMB1tn is on the cards.

So, via Long, to the notion that while Zhou

pledged to achieve “capital account liberalization,” he did not promise full

capital account convertibility. Expect a future of monitored flows and capital

controls where necessary even as China says it has opened the CA. Which should

surprise nobody, tbh. Per Deutsche, “capital account openness is not a bipolar

choice. Instead, it is a spectrum.”

So, as Long says, “managed convertibility” is

the more appropriate likely term — and it’s not as if the world’s

orthodox economic institutions, like the IMF, disagree with a cautious approach:

So what will China’s capital account look like under the future of

“managed convertibility”? We think there will be three themes in the coming

reforms.

First, access to domestic capital markets will be greatly increased, as

separate small quotas for each investor are replaced with large quotas for all

foreign investors in aggregate. The Shanghai-Hong Kong Stock Connect program marks the

first step in this direction. Previously, foreign investors only had access to

the Chinese financial market through an individual QFII quota. Although these

quotas have been increased quite a bit, they are still not large and investors

complain that the approval process is quite cumbersome. The Stock Connect

program instead has a RMB250bn quota for everyone, requiring no prior

approval—and the quota can be easily lifted when desired. A complementary

Shenzhen-Hong Kong Stock Connect program will also be launched later this year,

and we expect more such measures in the future. And in talks with the US in

June, China said it would create a similar program for the interbank bond

market, offering foreign investors an aggregate quota without individual

limits.

Second, as China liberalizes it will try give to preference to

longer-term investors who can be a stabilizing influence. A good example of this is its strategy for the bond

market. We expect the domestic government

bond market will grow rapidly in the coming years as fiscal deficits expand and

more local government debt is restructured… This gives the government an

incentive to open up of the bond market in order to find new marginal buyers of

bonds. The

potential is clearly very large: currently foreign investors hold just 2% of

China’s onshore bond market. By comparison, India allows foreign investors to

hold as much as 12% of its bond market. The People’s Bank of China said this

week that central banks, sovereign wealth funds and international organizations

can invest in the interbank bond market with no quota restriction, but

shorter-term investors did not get the same treatment. The recent stock market crash may also lead

regulators to restrict short selling and margin financing by foreign investors.

Third, restrictions on Chinese people moving their money outside the

country will be relaxed, but such flows will still be closely monitored. We expect the government will lift or remove the US$50,000

annual cap on foreign-currency exchange by households. Instead the central bank

will monitor the overall direction of flows and reserve the right to put on

more controls when necessary. There are domestic media reports that the central

bank will start pilot programs to test a removal of this limit in a few cities.

In its June report on renminbi internationalization, the central bank pledged

to provide an expanded channel for households to invest in overseas securities,

dubbed “QDII2.” Though details are scarce, it will be easy to improve on the

current QDII program which limits investors to a few Chinese funds and has not

been very popular.

Taken together, these changes have major implications for financial

markets: there is no question that capital flows into and out of China will

substantially increase. But there is also no question that China will declare

that it has achieved capital-account liberalization while retaining more restrictions

on capital flows than other major economies, and that it will not meet the

definition of full capital-account convertibility. This is not a criticism: we think a headlong rush to a

completely open capital account would be pointlessly risky. And this “managed”

approach will still get China what it wants: recognition that the renminbi is a

major global currency and that Chinese financial markets are of global

significance

This is all obviously educated guesswork from

Long but, even if he is potentially being a bit optimistic, the broad strokes

feel right.

China will want to bring money in for the

reasons outlined above — and as Pettis has said it will probably succeed in doing so

as yield hungry investors are attracted to RMB debt with the SDR push being used as potential cover — but it will be far more

reluctant to let it leave. Really reluctant,

(really) hypothetically.

Of course it remains to be seen how China’s

recent attempt to save/ destroy its equity market will hit demand more broadly,

but why anyone would expect any other form of liberalisation from China is

somewhat beyond us.

Related links:

China’s holy trinity and the

need for RMB stability –

FT Alphaville

China widens foreign access to

bond markets –

FT

China’s plan to deal with its

debt mountain –

FT Alphaville

China and a friendly reminder

to keep watching those capital outflows – FT Alphaville

http://ftalphaville.ft.com/2015/08/26/2138542/making-chinas-fx-reserves-feel-inadequate/